After two years of contraction, the EUROCONSTRUCT network expects the European construction sector to have entered a phase of cautious stabilization in 2025, marking the beginning of a gradual market adjustment.

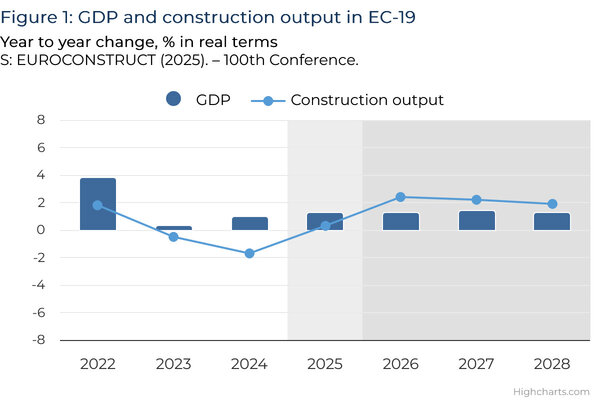

After two consecutive years of contraction, Europe’s construction sector is entering a phase of cautious stabilisation. According to the latest November 2025 figures and forecast from the Euroconstruct network, total construction output across the 19 member countries declined by 0.5% in 2023 and by 1.7% in 2024, marking the weakest two-year performance since the pandemic. Yet the outlook is shifting: the year 2025 should have ended with a modest growth of +0.3%, followed by a more noticeable expansion of +2.4% in 2026 as financing conditions ease and civil engineering becomes the main engine of recovery.

Economic fundamentals remain mixed. While interest rates have retreated from their 2023 peaks and inflation has moderated across Europe, construction activity continues to face strong headwinds: high building costs, affordability constraints, subdued private investment and persistent macroeconomic uncertainty. These pressures weigh most heavily on building construction, particularly the residential segment.

Slower recovery in the residential sector

According to Euroconstruct’s analysis, residential construction remains the primary drag on overall growth. New residential output dropped in 2023 and in 2024. A genuine rebound will materialise only in 2027. Residential renovation, also softened in 2024, declined again in 2025 but will return to modest growth in the following years.

This confirms a structural pattern: renovation remains resilient but no longer delivers the strong counter-cyclical support seen during the energy-efficiency boom of earlier years.

Rising demand in the non-residential sector

The non-residential sector is performing somewhat better. After a small contraction in 2024, growth returned in 2025, accelerating in 2026. The composition of demand, however, is changing. New non-residential construction is revised downward in 2025, reflecting cooling demand in commercial, industrial and logistics facilities amid slower economic momentum. Renovation for non-residential buildings remains the foundation of the sector, rising in 2025 and in 2026, supported by energy-performance requirements and the upgrading of ageing public and private facilities.

GDP and construction output in Euroconstruct-19 Area (Year to year change % in real terms)

Civil Engineering remains the strongest segment

By contrast, civil engineering remains the strongest and most stable component of the European construction cycle. After growing in 2023 and in 2024, the sector is forecast to expand in 2026, with both new infrastructure and renovation contributing. New civil engineering work is projected to grow, while renovation records a solid growth through 2028. The sector is set to stand really above 2023 levels by 2026, driven by transport investment, energy-transition infrastructure, climate adaptation and EU-funded programmes.

Divergent trends across countries

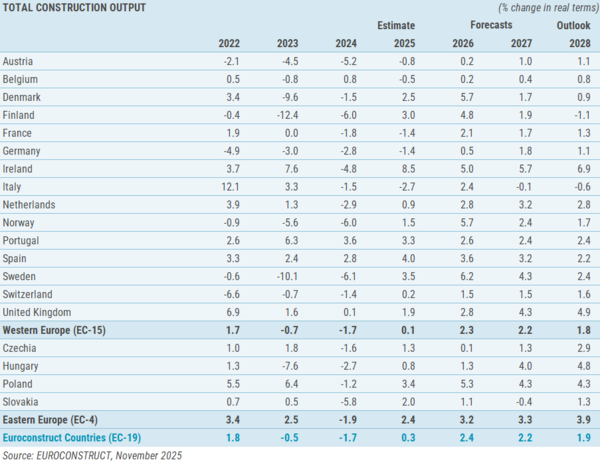

National trajectories remain highly heterogeneous. Only four countries – Ireland, Poland, Sweden, and the United Kingdom – will exceed 4% annualised growth between 2026 and 2028.

Among major economies, Spain shows solid prospects with 3.0% annualised growth, while France and Germany remain subdued at 1.7% and 1.1%. Italy grows only 0.6%, despite a significant upward revision from earlier expectations. At the lower end, Belgium (0.5%) continues to face stagnation.

Ireland stands out as the fastest-growing market through 2028, supported by strong public investment and resilient demand. Poland also posts strong medium-term growth despite downward revisions, while Spain and Portugal benefit from broad-based expansion in both building and civil engineering. In contrast, Germany, Austria, France and Italy face continued headwinds due to weak residential demand, high costs and constrained financing.

Evolution of construction output in the Euroconstruct area

Growth dynamics

One of the clearest outcomes of the November 2025 forecast is a shift in the composition of growth: new construction and civil engineering will increasingly drive the cycle from 2025 onwards, while renovation –still stable – enters a phase of lower expansion as fiscal constraints tighten and major subsidy programmes are scaled back. Total construction output will exceed 2023 levels by 2027, although the recovery remains uneven and sensitive to ongoing economic uncertainty.

Overall, the Euroconstruct network forecasts a gradual recovery. The combination of improving financial conditions, long-term infrastructure programmes and sustained renovation demand should help stabilise the sector in 2025 and support broader growth from 2026 onward.

Stay updated on the industry with curated data and insights each month: subscribe to the TECNA Magazine

POWERED BY CWR

PUBLICATION

24/03/2026

Other related news

20/08/2025

Industry and the challenge of artificial intelligence

04/02/2026

Advanced mineral solutions for large slab production

16/02/2026

The sustainable transition in the field of ceramic body preparation

22/04/2026

Algerian construction industry on the rise

12/05/2026

The Smart Factory: how to simplify complexity in ceramic production

24/06/2026

The Italian ceramic industry is worth €7.5 billion

17/09/2025

The future of construction in Europe between recovery and uncertainty

15/10/2025

Heavy clay machinery: the Italian industry holds its ground in international markets

14/11/2025

Clay building products: trends and figures of the Italian industry

04/12/2025

Not just large formats: the digital revolution also embraces special pieces

10/12/2025

World production of ceramic tiles

12/12/2025

The global exports of ceramic tiles decreased to 2.67 billion sqm in 2024

15/01/2026

The Italian tile industry ends 2025 on a positive note

26/01/2026

Ceramics take center stage in the “total look” of living spaces

19/03/2026

TECNA at Expo Revestir: securing a presence in key markets